The dollar is the most often used thing of value in which non-USA countries store their foreign currency reserve. First off, what’s a foreign currency reserve? These are often large sums of currency held by the central banks of various countries to stabilize their currencies. If there’s a sudden shock on the Swiss Franc, the government of Switzerland can buy or sell dollars to mitigate the shock. In some cases, the governments also use reserves to facilitate trade or government purchases. This was traditionally done with gold and silver. However, since 1974, it has largely been done with dollars. Dollars provided by a country that (until recently) was committed to international rules and institutions that facilitated trade and rule of law for disputes.

The dollar is not only a reserve, held by many countries including China and Russia, but also a preferred currency for many international exchanges. When you buy a barrel of oil, that contract is denominated in dollars. (Even though the Saudis did poke Joe Biden in the eye by executing some contracts with China in Yuan – it was a political move, not based economics). If a large bank, or a government, lends money to another country, it will generally do so in dollars. A German bank does not want useless Bolivars, Dinars, Pesos, Drachmas, or Rials. They want dollars, Euros, and Swiss Francs (probably in that order). The country or government receiving the loan also wants dollars. (Although Euros can be fine, as they translate quickly and easily into dollars).

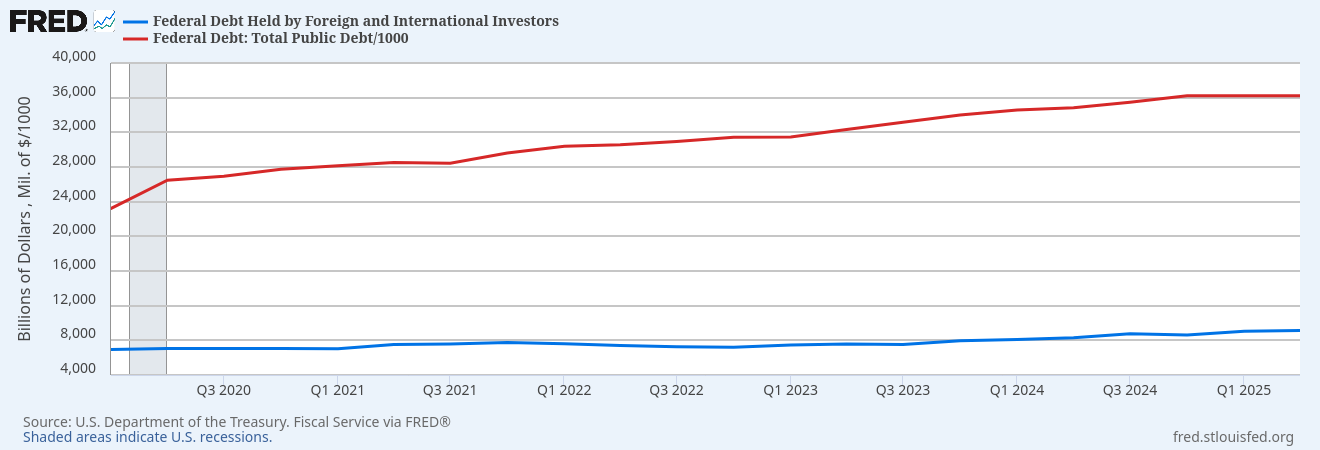

This puts the United States in a unique position, as the world’s supplier of dollars. When we run a deficit, we borrow that money in dollars. If a German bank buys a US treasury bond (a loan to the United States government), it will be repaid in dollars. The repayment risk to the German bank is minimal, as the US can just print all the dollars it wants. The risk to the German bank is the US will be poorly managed, and the value of the dollar will be inflated away. Let’s say the German bank buys the treasury bond for $1,000, expecting to receive $50 in interest every year for the next five years and then the $1,000 principle. At a 2% inflation rate, that $1,000 will be worth about $900 in today’s money. But if the US engages in some very stupid decisions, and the inflation rate climes to 5%, that will be worth $775 in today’s money. Until recently, the US has had largely very sober, responsible economic managers, so the risk was minimal.

How bad can inflation get? We’ve had 5% inflation for short periods at numerous times. It didn’t really bother people that much, because it quickly fell back down. We had around 9% under Biden for a brief period and people lost their minds. But many places have seen inflation rates in the 20% or more range for prolonged periods of time. They still survived as countries. Even hyper-inflated countries have held together. At a 20% inflation rate, the German bank would see $325 returned in today’s money. If that bank had any real fear the US was going to 20% inflation, they’d avoid the bond until it had over a 20% interest rate. But most US debt is actually held by US individuals.

On net, this is a good position. If we want to buy something we make the magic tokens most people want to exchange. If we need more dollars, we can make more. We don’t even have to print them. We just put some numbers in a database. People are also willing to buy our debt, which we will pay back in those same magic tokens we make. Unless we do something stupid, that results in protracted, high inflation, we will continue to hold this unique position. The contenders for this rare status are the Euro and the Yen. No one wants Yuan or other BRICs currencies, not even the BRICS countries. Many countries hold a basket of currencies that include Yen, Euros, Swiss Francs, gold, and silver, but the US dollar is the workhorse currency.

There have been a couple of recent incidents, however, that may interfere with the dollar status. The first is seizing reserves. Specifically, a federal court seizing Argentine dollar reserves held in the US to pay creditors. For any country relying on the auspices of the Federal Reserve to hold their reserves (which many countries do), the chance they are seized by a US court has to be taken into consideration. (The US also holds the gold reserves of other countries as well). Unless you want to have palettes of $100 bills in a warehouse, you may want to hold bearer bonds, gold, and silver in your own country. Along with this was partially pushing Russia out of the financial system for the invasion of Ukraine. Although this was something I felt was necessary at the time, with the recent administration, European countries especially might be concerned. Could UK assets be seized if the UK does something that insults the orange idiot? Before now it was assumed that it would require a lot of legal mumbo-jumbo – but with the administration operating outside the law, it becomes a matter of fiat by the generalismo.

What would the world do? I really don’t know. The idea of crypto currencies stepping into this role is ridiculous. The volatility of any crypto makes holding it as a reserve nearly suicidal. Likewise, gold seems unable to handle the requirements of a much larger trading system than pre-1974 trade. It would also be a boon to the Russians, something many Europeans would rather avoid. However, as we’ve seen, gold has been been climbing steadily over the last year. And it’s hard to detach the timing from the chaotic nature of US policy. The Euro and the Yen are not there yet in peoples’ minds. The Yen may be closer to that role than the Euro, which seems too susceptible to political meddling from Europe. (Which should be a warning to the dollar).

What would happen to the US if the dollar no longer occupied its current position? I think it matters how we get there. If we get there because of an orderly move to more balanced baskets of reserves, not much. But, if we get there because of dollar weaponization or severe inflation, that’s a different story. For one thing, we would be paying higher interest rates on US debt. If it’s an inflation story, both US and foreign bond holders would want higher interest payments. Somewhat less if it’s a weaponization story, but they still would want compensation for added risk. The dollar would fall in value as people demand less dollars. As a country that imports quite a bit of stuff, this would push inflation.

But I suspect the biggest change would be the world no longer has to “grin and bear it,” when the US does something they don’t like. On one side is a fall into policies that degrade the value of holding dollars On the other side is a fall into the world of inflation. Maybe it isn’t a tight rope. Maybe it’s more like a balance beam, with more room for error than I believe. But at the end of the day, the loss of the dollar’s special position would not make America great again.