Under what scenario does cutting rates, along with heavy deficit spending, not lead to inflation? If productivity expands from AI and automation. Setting aside my disbelief in the mechanics that would allow this to play out in a short-term basis, it is reminiscent of the supply side argument from the 1980s. You’ll still find people who believe in the argument to this day, even though the evidence has eviscerated it. But let’s hop into the way-back machine to 1980-something.

The argument was that inflation was a result of demand suddenly outstripping supply. If you lower taxes or raise spending, you stimulate the economy (that was when congress was not so politically deranged they couldn’t raise taxes to slow the economy, if needed). Other levers could be using the reserve requirement to stimulate or depress lending or raise the federal funds rate. By the early 1980s, and a brutal several months of extremely high rates, inflation was on its way down. But an interesting phenomena was emerging. The Philips curve, the statistical relationship between unemployment and inflation, began to ratchet up. For the same level of unemployment, it seemed like we were getting higher levels of inflation.

The solution was to push out the supply curve1. And if the solution sounds similar to every single Republican proposal you ever hear, it’s because it is. Cut taxes, especially among the investing and business class, and remove the pesky red tape, safety regulations, and environmental regulations. That would “unleash the animal spirits” of American enterprise and the supply curve would be pushed out to achieve higher levels of output (lower unemployment) without inflation. Well, we did cut taxes and Regan and trigger what (at that point) had been record deficits.

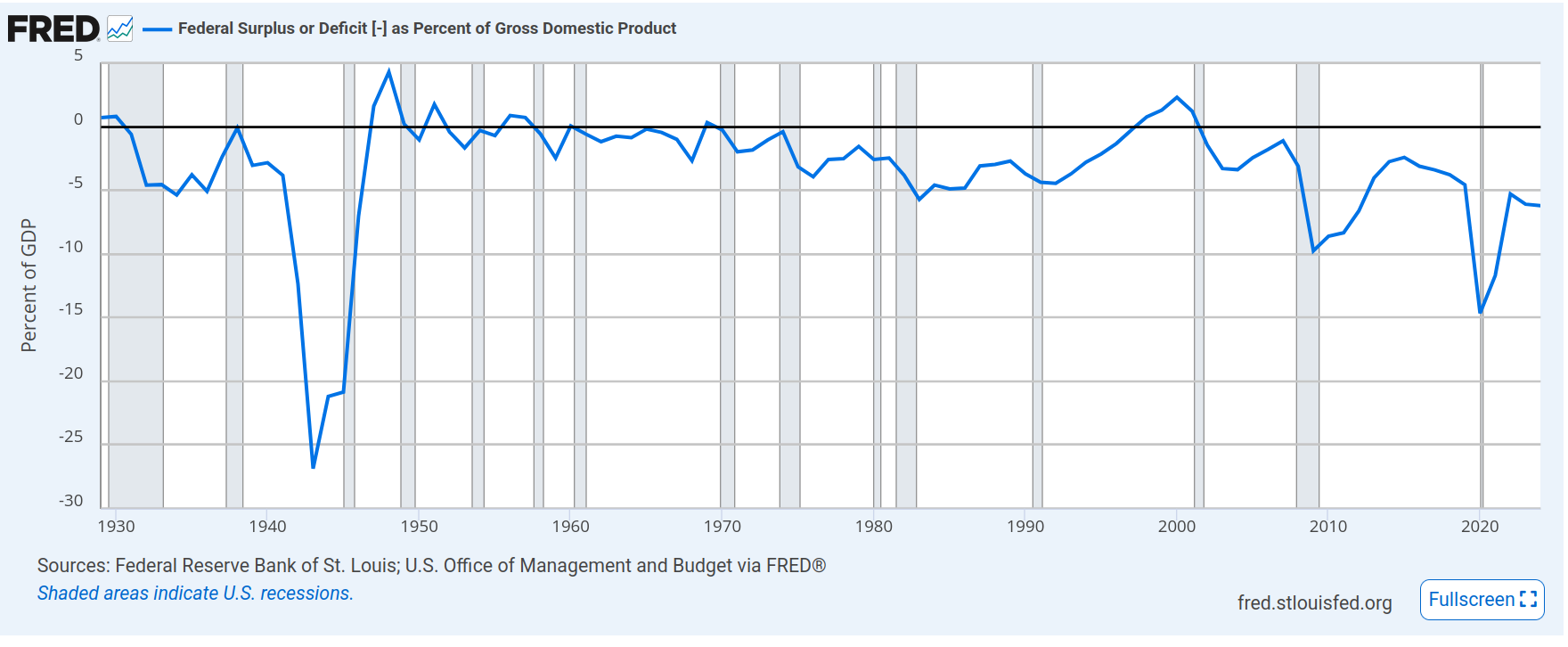

As we can see, except for World War II and the great depression, we’d never seen deficits so large as under Regan. And now we can’t even get to striking distance of a surplus. But that’s okay. We’ll have deficits now, but the economic activity will make up for it, right? Meh – not so much. They say George H.W. Bush lost the 1992 election because he broke his promise of no gnu taxes. And I beg to differ. Neither yaks, gnus, oxen, or other ruminants had their taxes raised. Under the profligate Democrats, from 1992 through 2000, deficits actually shrank and we had a surplus. Until the next Republican figured out how to drive massive deficit spending again (and almost put is into another great depression – but that’s a story for another time).

Any economist, in the 1980s, believed the supply side of the demand and supply curves could expand out, achieving greater well-being with limited changes in the price level. It just took time. It takes time to build a factory or get a business running. Because of improvements in technology and productivity, over a period of 5, 10, or 15 years, the supply curve slowly pushes outward.

That wasn’t the supply side argument. It argued that you could drive the supply curve to higher levels of productivity in the short term, without inflation. Not 5 or 10 years, but 1 or two years. Tax revenues would shoot up and cover the short term deficits. But, at the end of the day, there was no great well of untapped capacity in the United States that would have allowed such an expansion. And low and behold… there was no great increase in production and deficits went up. To avoid inflation, Volker had to keep rates high and jack up the Fed Funds rate again. No great swell of tax revenues came in to fix the deficit issue.

But the 1980s were a decade of great prosperity and economic growth, right? Yes, as the Fed and the administration and congress had dueling economic policies. The don’t tax but spend a lot policy of the Republicans had to be throttled by the interest rate policy of the Fed to avoid a return to high inflation levels. Maybe Volker should have just said “fuck it” and let the deficit spending result in massive inflation, but he kept the brakes on. So yes, the 1980s was a great decade because we mashed the accelerator and the brake at the same time, but just so the car could move forward.

The argument evolved from the short term variant to a new variant (much like COVID) that was more congruent with reality. That was the long term supply side argument. “See, we were right, the supply curve eventually did shift right.” Over a period of several years, just as many economists would have argued before the ill-conceived economic experiment. Their revisionists argue it was about long term movement of the supply curve, you just mis-understood us on the short term stuff. That’s not an evolution of the argument to take into account new realities, but rather how intellectually dishonest people (liars) cover their tracks.

Which brings us to the present. The president wants to do what Regan never would have dared, because Regan believed in America and American institutions. He wants to make the Federal Reserve a tool of the administration. He wants them to drop rates at the same time he’s engaged in deficit spending. (And like any good autocrat, skim a little off the top and drop it in an account in Qatar). The claim is there is a great untapped reserve of unproductive people who could be rendered so much more productive, that we’ll get more output at the same level of prices.

This argument is completely predictable. Lower taxes, lower regulation, and lower rates and the economy will blossom. The magic will be AI that will suddenly allow people to produce so much more that the increased demand will be satisfied at the same price level. We’ve had AI in various forms for a few years now. We are not seeing any change above the historical bounds for productivity. In the last couple of years there hasn’t been any sign that productivity is being impacted at all. In fact, computers have coincided with a drop in productivity since their wide-spread introduction in the 1970’s. But that was a key to the supply side argument as well, the animal spirits would be unleashed, in part, through productivity.

I want to be clear that in the 1980s I believed the argument the supply side economists were making. I’m writing this, as someone who took the argument seriously, looked at the outcome, and then realized the argument was wrong. And I see why it didn’t work, and never would have worked, even if Volker had dropped rates. I look at it this time and see the same argument being made, except by clearly worse people. We drop taxes on (disproportionately) the wealthy, we lower safeguards around our safety and health, and now we drop interest rates (which will cause the assets of the wealthy to inflate), and we’ll get this ground swell of growth without inflation. We are making the same mistake, twice.

That takes me to my next topic, which is the Iran strike. Now we have a 10 to 15 day timeline. That puts it in the range of March 2 to March 7. The next new moon is March 18. However, as I explained, that doesn’t matter if the moon is set. Moon set, however, will be between 6 AM and 8 AM, meaning there will be moon all night, with March 3 being a full moon. Darkness is good for US operations because we’ve focused on being able to see at night, something that’s expensive and out of the reach of many militaries. The darker it is, the harder it is to spot planes, helicopters, and drones. The next good opportunity after March 7 is about a week later, March 15. March 15 is a Sunday, so the strike would get full Monday morning news coverage. Beware the ides of March?

- I should state, for clarity, that there are no Supply and Demand curves. It’s a pedagogic tool used to explain concepts around issues like how economic output and price level interacts. That sometimes the nominal growth you see comes in the form of inflation and not more goods and services. ↩︎