The Jobs number came out weak. PPI came in hot, recently, Jobs weak, that means STAFLATION!

As the US has attempted to close its border to new migrants, and the incel kids can’t make a baby with their AI waifu girlfriend, we aren’t growing. We’re aging. That means, on net, fewer workers between 18 and 65 available to work. This can be moderated with more people delaying or deferring retirement, but not much. Unless we import new people or we make more, we are going to have a shrinking labor pool, a growing population of old folks, and fewer young folks to keep the system going.

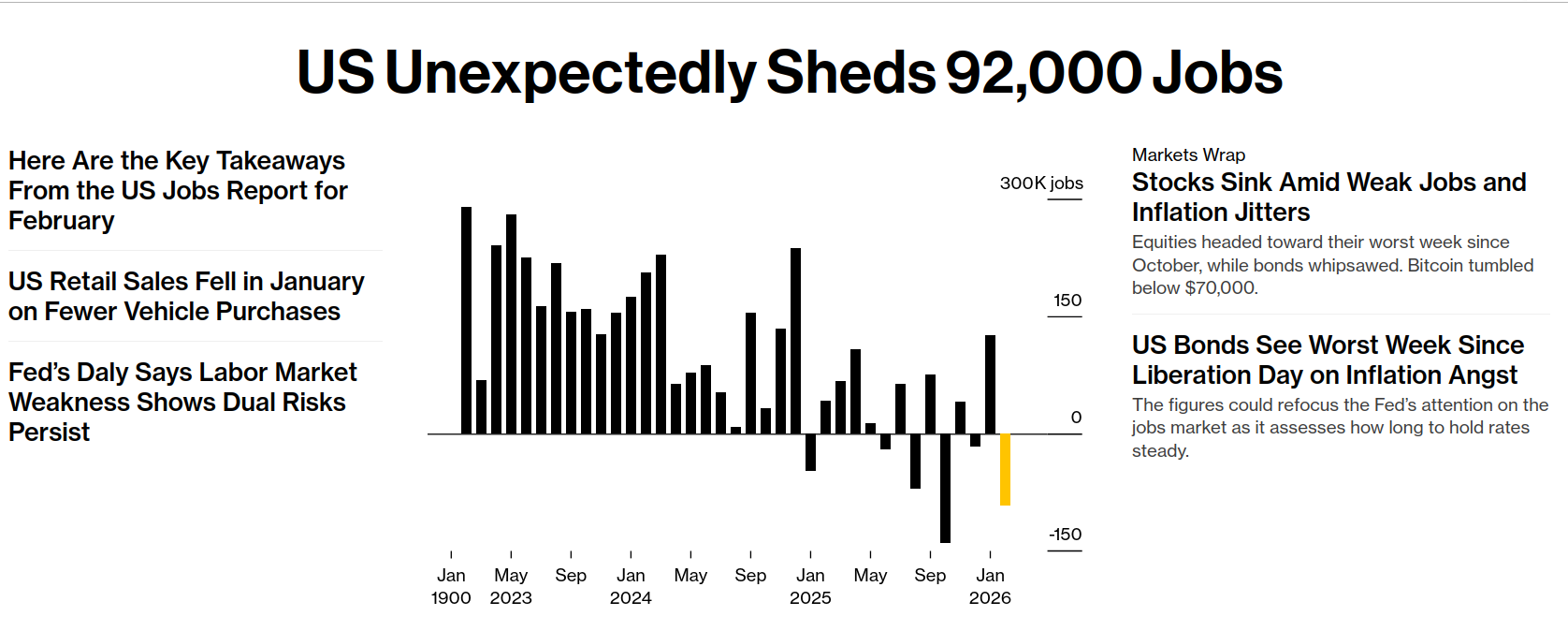

Next is the jobs number itself. It’s been subject to wild swings up and down with revisions. People pussy-foot around the issue, but I think it’s right-leaning assholes being assholes. I know it’s going to be hard to believe, but even politically “independent” business owners lean right. And the right wing idiot-sphere thinks answering questions from the government is a violation of your rights. I don’t think they lie, and I don’t think they just say “I ain’t answerin’ no guv-oh-ment form.” I think they just don’t make it a priority. Or a priority to get right. So we get revisions.

Are we moving to stagflation? I don’t know, but it’s definitely on my radar. Especially if we get inflation shocks from oil being elevated for several months. It’s not only the war, but the falling dollar is likely to push the price of all commodities up for Americans. Although the war of unnecessary stupidity is kicking the phenomena into high gear. We could wind up with a lot of inflationary pressure, keeping rates high, but no growth.

If the jobs numbers are consistently negative, we’re moving toward stagflation, if we’re lucky. That would mean we don’t aggressively escalate unemployment, everything just gets increasingly ‘meh.’ In the bad scenario, like the AI bubble deflates and the spending power of the top 20% along with it, we wind up with recession. Something which we will have limited tools to handle. With the deficit as high as it is, and Democrats may not be checking addition defense spending, fiscal policy may not be there. And monetary policy may just stimulate inflation more than growth (which is a back-handed way to default on the value of our debt).

One thing you can do by bringing down rates is to goose the economy by jacking up asset prices again (good for that top 10%), and that would counter the wealth effect problem. But it risks an inflation problem as you are effectively printing money by increasing credit. And dropping rates, drops the dollar, which pushes up the cost of commodities (like oil). So the people who benefit least pay more for gas and food, while housing gets further out of reach.

Are the numbers indicative of a problem? I don’t know, we’ll have to wait for the revisions. But a string of bad numbers would not be a good sign. But we also have to keep in mind the lack of population growth, aging population, and therefore shrinking labor pool. We could create zero net new jobs this year and maintain full employment. The economy could even grow at that point, with a long term growth curve the sum of productivity games minus the shrinking population. It would mean that companies have to work a lot harder to make a 10-15% growth target, with a 5%-10% growth target looking more manageable. That lowers the multiples on those companies, the price of their stock, and oh-oh… the top 10% stop spending to compensate and we’re back to recession.

If we want to close down immigration, just age in place with no new blood, might just have to face the fact we’re not the spring chicken we used be. And if we think AI will be a huge productivity boost, we haven’t seen it yet. That’s not that it might not happen, but it could happen at a much higher price-point to sustain the costs companies and utilities will pay. In which case its effect will be tempered by economic reality. And if we don’t get a jump in productivity, we’ll wind up just kind of puttering about 1% long term growth. Wait… If long term growth (usually assumed to be population growth + productivity growth) is 1%, where does inflation need to be to keep our living standards in place. It needs to be below 1%. I don’t know where 1% inflation is on the Philips curve right now, but it is not at 4.4% unemployment.

We would need AI to power a 2.5% or better productivity growth to retain our 2% target inflation rate and not go into a slow decline of living standards. So, far, productivity figures are in the normal range for the last 40 years. So yes, don’t worry too much about one bad number. Worry a lot if we get a string of bad numbers, keeping in mind we can live with zero net job growth. But those numbers could all be corrected away in six months. But also worry a lot about what a fixed population means for long term growth. And what it means for living standards long term. So yeah, panic, but don’t panic.

This is not investing or investment advice to you, or anyone. It’s is provided for your entertainment purposes only. And if you are investing, contact a professional before making any decisions. Buying and selling stocks, futures, or any investment is a risky activity and can cause you to lose money, including the principal which you invest.