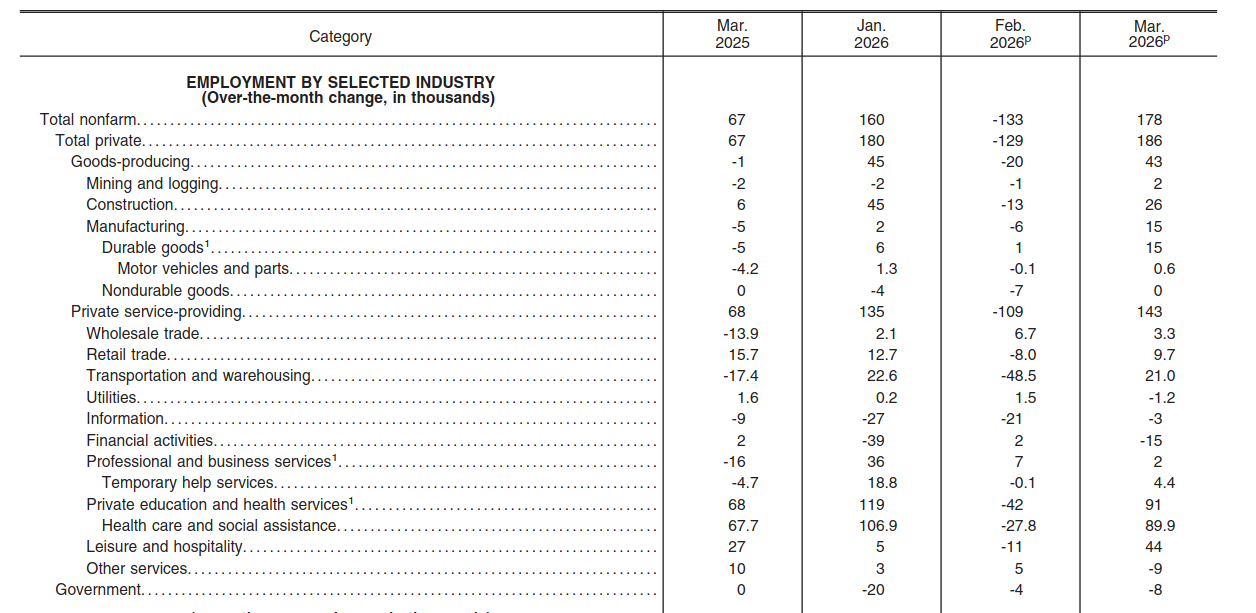

The jobs report came out with a spicy 178,000 jobs created, after last month’s [insert sad trombone], job losses. Looking down the list, the bulk of the jobs came in from health care, leisure, and transportation. Health care might be creating a lot of jobs as baby boomers start arriving at their 80s, but health care workers can be low margin jobs. While it may produce jobs, it may not produce investment opportunities. And like many difficult, uncomfortable jobs in America, it is largely staffed by immigrants, against which the current administration has initiated a pogroms as part of ethnic-cleansing lite. Construction, likely because of data centers, did fairly well. With information and financial services being the biggest losers.

Of course, as we’ve seen, the jobs report can be subject to a lot of revisions. A quick scan down indicates the revisions for January were a +27% change, while February a -45% change. Which is actually the opposite I would have expected, with large deviations from the mean pulling back to the mean as more data comes in. This means, until March is revised, we stand a net 171,000 non-farm payrolls for the year. Meaning we created just under 60,000 jobs a month. If we had a normal influx of immigrants increasing the population (many arriving already working age), that would be medium bad. But with no population growth, it’s likely a good number. Prior to the current hell-scape, we needed 100,000 to 150,000 jobs a month to absorb new entrants.

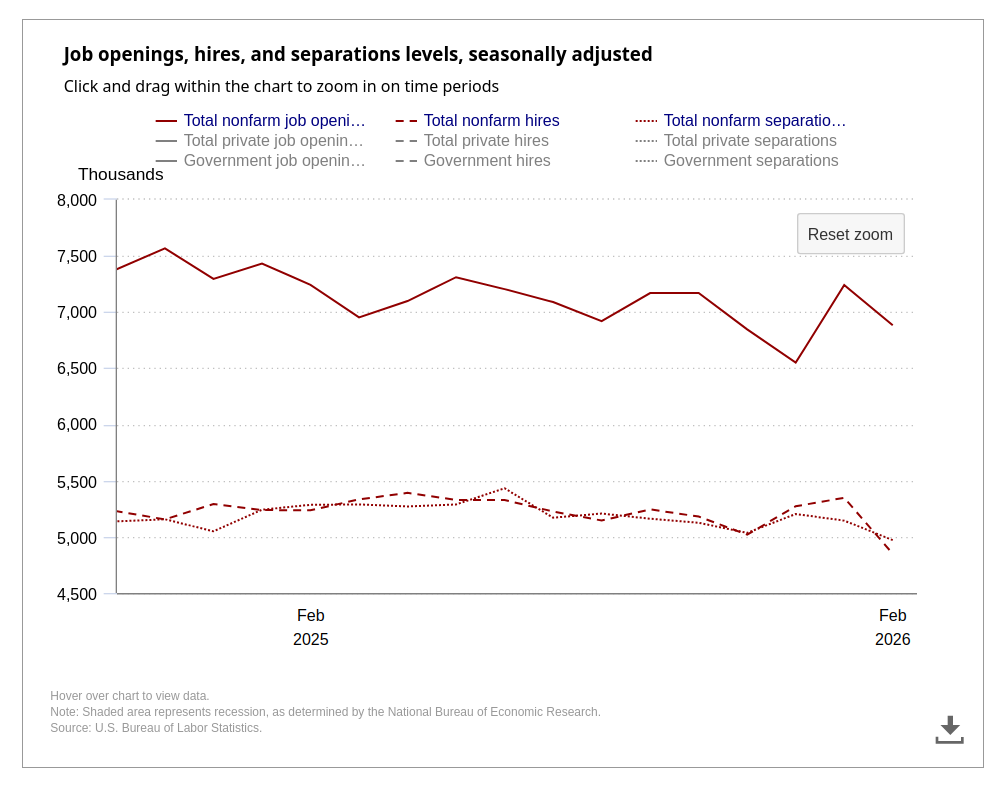

To get some context around the jobs report, let’s look at JOLTS, which only covers up to February (jobs data covers March). We see, in fact, February was a rough time. With openings, quits, and hires, all trending down, indicating it’s harder to lose a job and harder to find a job. This is in line with anecdotal stories about businesses being slow to fire (after spending months unable to hire just a couple of years ago). And in line with job seekers, especially new job seekers, finding limited opportunities.

What does this mean for interest rates? And that’s the real question, isn’t it? Does Jerome Powell and company reduce rates? It’s motivation to reduce rates at some point. If our economy adds 60k jobs a month, that might be more than adequate with a stagnant population, but historically ‘meh’. But it does not scream bad labor market as February’s job report did. And with oil going through the roof, combined with tariffs finally(?) biting, the pressure may be to hold rates. I don’t think there’s any serious talk of raising rates. Maybe if inflation went back to a the high-side of a 3 handle?

We’ll have to watch the CPI, over the coming months, as higher oil prices work their way through the system. We also don’t know how the oil shocks will play out. While Americans rend their garments and gnash their teeth over a dollar per gallon (0.25 per liter) change in pricing, countries in Asia have to decide if the limited supply they receive will go into making Tupperware for said Americans, or they have keep their infrastructure going. Countries throughout Asia, where Persian Gulf oil flows, are looking at rationing. For them it’s not about paying more, it’s about availability.

Which would start other knock-on effects. Plastics and other products are made either from natural gas feed stocks or from petroleum. That can include, I recently found out, medicines, or the compounds that go into making medicines. The price for many things, ranging from Zip-Loc bags to the anti-depressant keeping you going for the next three years, may increase, if they are available at all. And then there’s the issue of fertilizers, which are also either shipped out through the Persian gulf or made with natural gas shipped out of the Persian Gulf. A second order effect, such as the supply of precursor compounds for medicines being interrupted, may be a massive crisis in its own right.

And while that’s on the horizon, we’re not there yet. And that assumes there isn’t and adjustment to mitigate some of these impacts. If the shooting stopped today, product would flow through the gulf. There would be less, until the damage from the war is cleaned up and halted production is restarted, but the spice would flow. And there’s no reason the shooting can’t stop right now. People just have to stop shooting. But they won’t, so as this drags on, more infrastructure gets damaged and restarting will be slower and more painful.

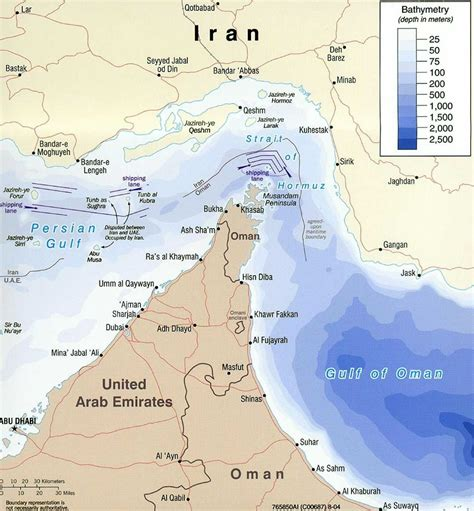

What was once my nightmare scenario may now be the outcome, and no longer my nightmare. And that is Iran turning the Strait into a toll road, with the ability to limit traffic for political reasons. Iran didn’t have that ability before the war started, but they might get it now. As there is no way, short of a ground invasion of a country of 90,000,000 people, who could fire missiles and drones from their mountainous region, to open the Strait without their cooperation. A country that puts religion and institutions over the comfort an survival of individual people, might decide to close the Strait every time Israel decides to bomb Syria or Lebanon (like every other Tuesday), or murder its ethnic minorities (which happens only on days that end in ‘y’). Or if the Jets don’t win the Superbowl.

The nightmare now is Iran and the US trade blows (including the loss of American Marines and paratroopers as the US tries to open the Strait by invading), and more and more infrastructure gets destroyed. And essentially zero oil flows until Venezuela can be ramped up. Which would take months, and possibly US help to provide security to the oil producers. The “new normal” in oil prices becomes $150 a barrel and fertilizers go through the roof (and sometimes aren’t available). But because the infrastructure needs to be rebuilt, when the shooting stops, it will be months before we see consistent supplies and maybe a year or more before we get below $100 a barrel. While the US goes through recession and is bogged down in guerilla fighting in Venezuela.

I would bet folding money that rate cuts aren’t on the table for the rest of year, unless the AI bubble implodes so hard it threatens systemically important banks (not likely). But it could take a couple of points of GDP and therefore jobs. Unless we get the Strait open soon, we might be looking at rate increases, unemployment to push toward 5% and inflation pushing 3-4%. The rate increases keep it from going to 5, 6 or 7%. (The OECD is predicting 4.2% US inflation). And Asia will be fucked. Countries from India to Japan may deal with uprisings with China making hay and inroads while the US fails to put out the fire it started. I also bet folding money that the Russian sanctions are loosened as a stop-gap, and Zilenskyy is threatened by the US if he keeps blowing up Russian oil infrastructure.

In the 1980s, coming out of the 1970s stagflation, people just “extended the line” and saw a world with same shit, but more extreme outcomes and better technology. This was the cyberpunk dystopia, which even predicted the global, omni-present internet. (We had bulletin boards and dialed around to send messages and post our stupid opinions even back then, plus universities had the web-free internet). This is not a future we wanted, because it was assumed we would get there on the backs of venal and incompetent politicians who favored wars and the rich over the welfare of the whole population. And while the Republicans have been obligingly providing said politicians, for the most part we’ve been competent. We don’t have to go down that road. We could stop shooting today, if one person wanted to stop.